10 Jun 2020 2019 shipments and 2020 outlook

COVID-19 General disclaimer

Due to the uncertainty that COVID-19 crisis brought to the global economy, the consumer demand and the industry dynamics, along with the limited view we had of its impacts as of April 2020, forecast figures at the time of publication are exceptionally limited. Eurosmart will review the market and secure element segments in October. The 2019 figures remain the definitive ones.

“Eurosmart confirms a mature worldwide market in 2019 for secure elements”

Financial Services

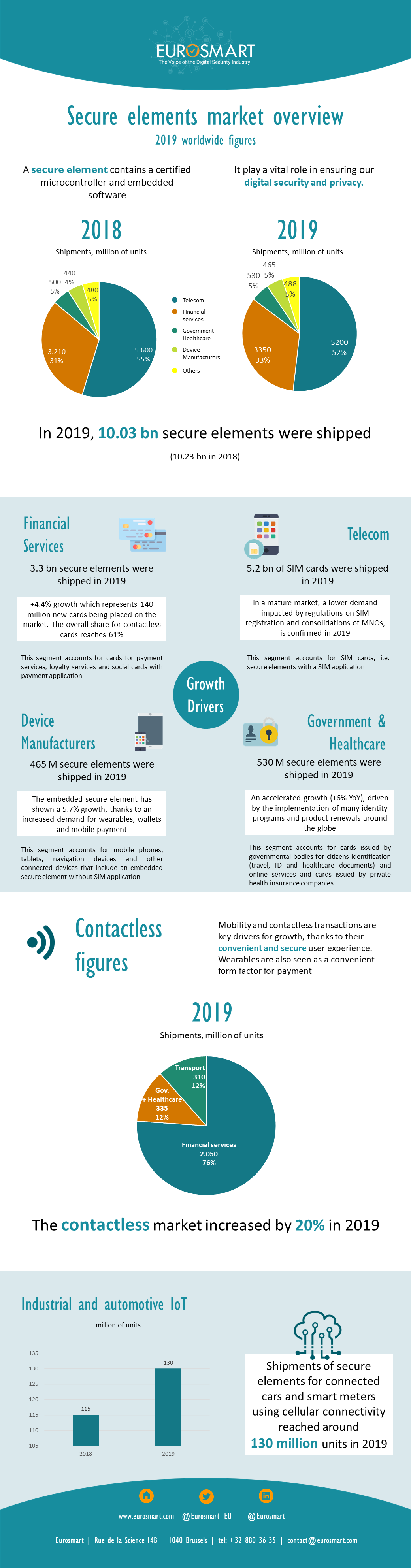

In 2019, the overall growth is confirmed at +4%, representing an additional volume of 140 million cards compared to 2018 figure, and reaching a global payment card production of 3.3 billion units. The market is driven by a strong demand from North America and South-East Asia thanks to a mix of renewal and migration. Fintech companies are also supporting the sustainability of this demand by increasingly providing card solutions to their growing number of customers.

During 2019, contactless cards were the main market driver growing at +24% YoY and reaching an overall share of 61%. Besides that, the deployment of broader contactless infrastructure smoothly fosters the increased demand of contactless technology.

In 2020, the recommended physical distancing measures to fight COVID-19 have contributed to promote the use of contactless payments (i.e. Contactless payment transaction limit has been raised in at least 60 countries). And while the total share of contactless cards is estimated to grow to at least 65%, it is also expected that EMV demand will suffer a contraction during this year.

Telecom

Eurosmart confirms a mature market in 2019, impacted by regulations on SIM registration and consolidations of MNOs. A lower demand is also confirmed in 2019 representing about 5.2 billion units shipped.

In 2020, demand decrease is expected to continue as the COVID-19 crisis is not only impacting mobile phone shipments but also modifying consumers’ buying behavior – e.g. through different product mixes, as well as extended smartphone renewal cycles— and closing the main issuance channels mostly in prepaid countries. In parallel, standardization efforts have been suffering from some delays.

The embedded UICC is expected to grow further; new products supporting the embedded SIM technology have been launched by 3 out of the 5 largest smartphone makers. This accelerated adoption of embedded SIM technology is driven by factors such as the standardization of remote provisioning. In 2020, Eurosmart foresees embedded UICC shipments to grow at double digits despite Covid-19. So far, Removable SIM and embedded SIM coexist on the market and in the device, thus a rapid or strong substitution is not observed, neither expected.

Device Manufacturers

In 2019, a positive trend noticed in most countries led to a total volume of 465 million embedded secure elements shipped. Mobile payment, wallet and wearables have been showing a continuing growth. For 2020, the growth depends on the depth of the pandemic crisis that currently impacts mobile phones demand and consumer behavior.

Government

In 2019, the sector kept an accelerated growth of +6% YoY, driven by the implementation of many identity programs and product renewals around the globe. The increasing number of cross border travels explains the demand of travel and identity documents during the year. The leading choice of governments for the contactless interface made it reach 63% share of 2019 shipments. This share is expected to slightly progress during 2020 amid an overall impact in demand of ePassport and ID document, and mainly due to deteriorated capability and willingness to travel during the pandemic.

Eurosmart also expects a push of the demand coming from the adoption of the 2019 European Citizen’s ID and resident cards format, which includes contactless interface. This growth is underpinned by contactless Identity documents that are now readable by a mobile NFC reader. Digital identity initiatives and programs contribute to the growth of secure element usage for private identities and online services.

Industrial and automotive IoT

A continuing growth for the M2M market is confirmed for 2019. This market is driven by a push for connectivity and embedded security in the automotive sector and other industrial segments. Shipments of secure elements for connected cars and smart meters using cellular connectivity reached around 130 million units in 2019. While long term growth is likely to continue, shipments in 2020 will depend on the resilience of certain industry segments.

Eurosmart estimated WW µP TAM – (Mu)

| 2018 | 2019 | 2019 vs 2018 % growth | |

|---|---|---|---|

| Telecom* | 5600 | 5200 | -7% |

| Financial services | 3210 | 3350 | 4% |

| Government Healthcare | 500 | 530 | 6% |

| Device manufacturers** | 440 | 465 | 6% |

| Others*** | 480 | 488 | 2% |

| TOTAL | 10230 | 10033 | -2% |

* MNOs (secure element with a SIM application)

** Device manufacturers represent Original Equipment Manufacturers of mobile phones, tablets, navigation devices, wearables and other connected devices without SIM application (Embedded Secure Element without SIM application)

*** Others include Transport, Pay TV, and physical and logical access.

Eurosmart estimated WW µP TAM – (Mu) Contactless

| 2018 | 2019 | 2019 vs 2018 % growth | |

|---|---|---|---|

| Financial services | 1650 | 2050 | 24% |

| Government Healthcare | 300 | 335 | 11% |

| Transport | 295 | 310 | 5% |

| TOTAL | 2245 | 2695 | 20% |

Eurosmart estimated WW µP TAM – (Mu) Industrial IoT

| 2018 | 2019 | 2019 vs 2018 % growth | |

|---|---|---|---|

| industrial IoT* | 115 | 130 | 13% |

*Industrial IoT: SIMs, eUICC, M2M form factors (MFF2, …) currently limited to M2M usage in automotive, smart meters.